Show Python code used for this comparison

# Portfolio Optimization

import os

os.environ['TF_CPP_MIN_LOG_LEVEL'] = '1' # or '3' to suppress even more

import matplotlib.pyplot as plt

import pandas as pd

import yfinance as yf

from dateutil.relativedelta import relativedelta

from tqdm import tqdm

from SpecificPortfolio.Training import Model

from TrainingSet import Data as Source

# See README file for project description

# _____________________MODEL INPUTS________________________

# >List of Securities

Securities1 = ['RY.TO', 'CNQ.TO', 'TD.TO', 'CM.TO', 'ENB.TO', 'SU.TO', 'BNS.TO', 'TRP.TO', 'AEM.TO', 'NTR.TO']

ETF1 = 'ZWC.TO'

Securities2 = ['SU.TO', 'ENB.TO', 'NA.TO', 'FTS.TO', 'TD.TO', 'CM.TO', 'GWO.TO', 'RY.TO', 'BMO.TO', 'CNR.TO']

ETF2 = 'XMV.TO'

Securities3 = ['RY.TO', 'TD.TO', 'SHOP.TO', 'AEM.TO', 'ENB.TO', 'BMO.TO', 'BN.TO', 'CM.TO', 'BNS.TO', 'CNQ.TO']

ETF3 = 'VCN.TO'

Securities4 = ['CLS.TO', 'SHOP.TO', 'CSU.TO', 'GIB-A.TO', 'DSG.TO', 'OTEX.TO', 'KXS.TO', 'BB.TO', 'LSPD.TO', 'BITF.TO']

ETF4 = 'XIT.TO'

Quarters = 10

InitialBudget = 1000

MaxSteps = 100 # <- Number of vector steps the model will go through until end of optimization

GROUPS = [

{"name": "Group 1", "securities": Securities1, "etf": ETF1},

{"name": "Group 2", "securities": Securities2, "etf": ETF2},

{"name": "Group 3", "securities": Securities3, "etf": ETF3},

{"name": "Group 4", "securities": Securities4, "etf": ETF4},

]

def build_etf_value(etf_ticker, quarters, budget):

data = yf.Ticker(etf_ticker).history(period="max")[['Close', 'Dividends']]

data.index = pd.to_datetime(data.index)

data = data.sort_index()

end_filter = data.index[-1] - pd.DateOffset(months=3 * quarters)

df_filtered = data[data.index > end_filter].copy()

quarterly_dates = df_filtered.index[::63]

dividend_payouts = df_filtered[df_filtered["Dividends"] > 0].copy()

initial_shares = budget / df_filtered['Close'].iloc[0]

current_shares = initial_shares

running_shares = []

# Accounts for compounding dividends through additional share purchases.

for _, row in dividend_payouts.iterrows():

div_shares = current_shares * row['Dividends'] / row['Close']

running_shares.append(div_shares)

current_shares += div_shares

dividend_payouts["DivPayouts"] = running_shares

df = df_filtered.copy()

df["DivPayouts"] = dividend_payouts["DivPayouts"].reindex(df.index, fill_value=0)

df.iloc[0, df.columns.get_loc("DivPayouts")] += initial_shares

df['cum_Shares'] = df['DivPayouts'].cumsum()

etf_value = df['Close'] * df['cum_Shares']

return etf_value, quarterly_dates

def run_group(group, quarters, initial_budget, max_steps):

securities = group["securities"]

etf = group["etf"]

etf_value, quarterly_dates = build_etf_value(etf, quarters, initial_budget)

model = Model(securities, max_steps)

calc_obj = model.CalcObj

optimized_value = []

budget = initial_budget

dataset, _, dividends, _ = Source.yf_Data(securities)

# Quarterly adjustments.

for quarter_date in tqdm(quarterly_dates.tz_localize(None), desc=group["name"]):

date_input = quarter_date + relativedelta(months=3) # aligns with calc obj processing

calc_obj.Specify(date_input, securities)

model.Features = calc_obj

weights = model.Train() # <= optimal weight for next quarter

dataset_filtered = dataset[(dataset.index > quarter_date) & (dataset.index < date_input)]

dividends_filtered = dividends[(dividends.index > quarter_date) & (dividends.index < date_input)]

indv_alloc = weights * budget

shares = indv_alloc / dataset_filtered.iloc[0]

portfolio = (dataset_filtered * shares).sum(axis=1)

divs = (dividends_filtered * shares).sum().sum() # total dividends over the quarter

# Budget at end of quarter will be ending capital plus accumulated dividends.

budget = portfolio.iloc[-1] + divs

# Add dividends accumulated to end-of-quarter portfolio value.

portfolio.loc[portfolio.index[-1]] += divs

optimized_value.append(portfolio)

total_value = pd.concat(optimized_value)

optimized_return = (total_value.iloc[-1] - total_value.iloc[0]) / total_value.iloc[0]

optimized_quarterly = ((1 + optimized_return) ** (1 / quarters) - 1) * 100

etf_return = (etf_value.iloc[-1] - etf_value.iloc[0]) / etf_value.iloc[0]

etf_quarterly = ((1 + etf_return) ** (1 / quarters) - 1) * 100

total_value.index = total_value.index.tz_localize(None) if total_value.index.tz else total_value.index

etf_value.index = etf_value.index.tz_localize(None) if etf_value.index.tz else etf_value.index

return {

"name": group["name"],

"etf": etf,

"securities": securities,

"total_value": total_value,

"etf_value": etf_value,

"optimized_quarterly": optimized_quarterly,

"etf_quarterly": etf_quarterly,

}

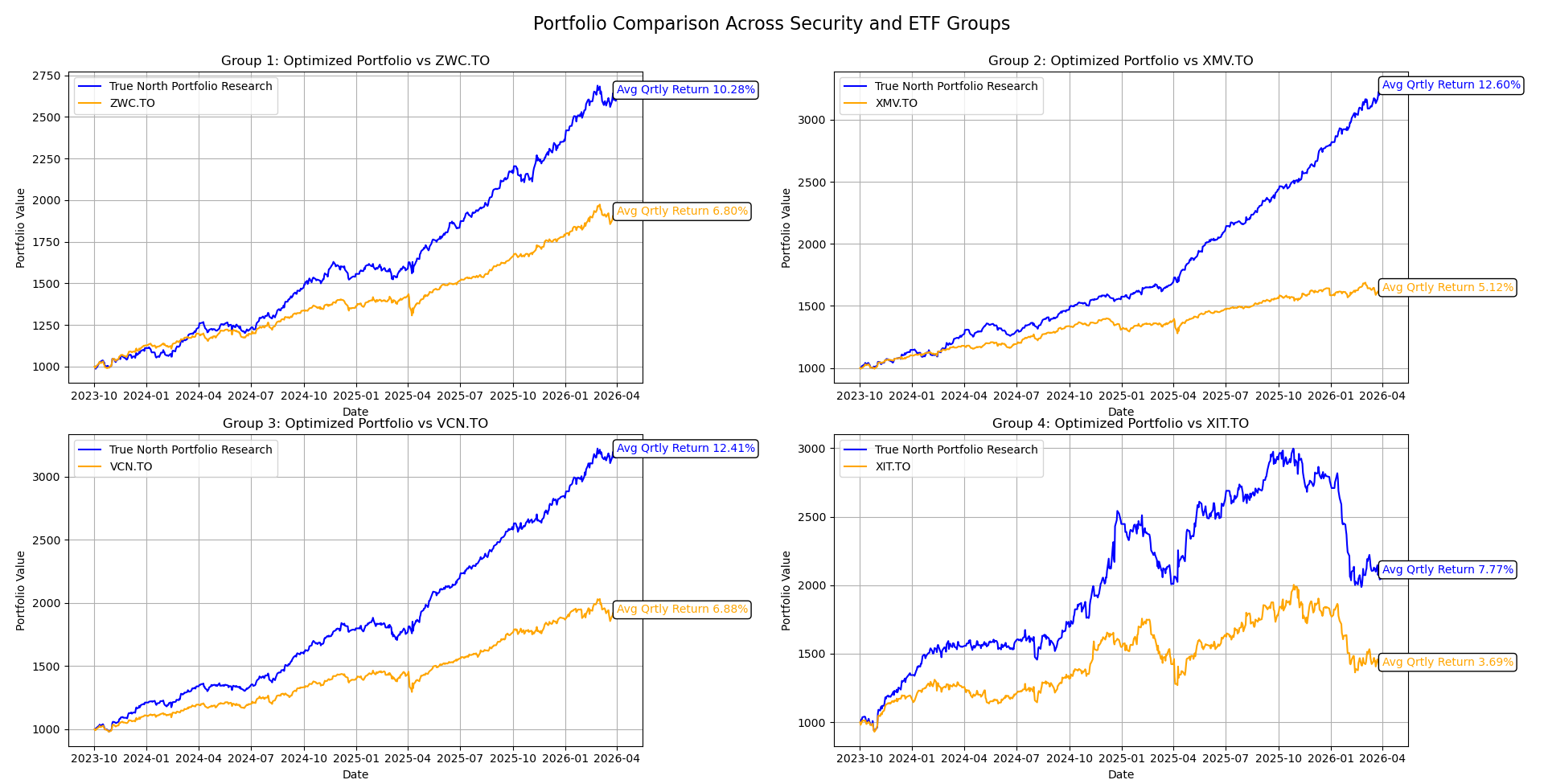

def plot_group_comparison(results):

fig, axes = plt.subplots(2, 2, figsize=(18, 12), sharex=False, sharey=False)

axes = axes.flatten()

for ax, result in zip(axes, results):

total_value = result["total_value"]

etf_value = result["etf_value"]

ax.plot(total_value.index, total_value.values, label='True North Portfolio Research', color='blue')

ax.plot(etf_value.index, etf_value.values, label=result["etf"], color='orange')

ax.text(

total_value.index[-1],

total_value.values[-1],

f"Avg Qrtly Return {result['optimized_quarterly']:.2f}%",

color='blue',

va='center',

ha='left',

fontsize=10,

bbox=dict(facecolor='white', edgecolor='black', boxstyle='round,pad=0.3')

)

ax.text(

etf_value.index[-1],

etf_value.values[-1],

f"Avg Qrtly Return {result['etf_quarterly']:.2f}%",

color='orange',

va='center',

ha='left',

fontsize=10,

bbox=dict(facecolor='white', edgecolor='black', boxstyle='round,pad=0.3')

)

ax.set_title(f"{result['name']}: Optimized Portfolio vs {result['etf']}")

ax.set_xlabel('Date')

ax.set_ylabel('Portfolio Value')

ax.grid(True)

ax.legend()

for ax in axes[len(results):]:

ax.remove()

fig.suptitle('Portfolio Comparison Across Security and ETF Groups', fontsize=16)

fig.tight_layout(rect=[0, 0, 1, 0.97])

plt.show()

all_results = [run_group(group, Quarters, InitialBudget, MaxSteps) for group in GROUPS]

plot_group_comparison(all_results)